Maximize Your Tax Refund in 2026: 7 Mistakes You’re Making (and How to Fix Them)

Tax season is here, and millions of Americans are leaving money on the table without even knowing it. The IRS has rolled out new rules for 2026 that could boost your refund significantly: but only if you avoid these critical mistakes.

After preparing thousands of returns for New Haven families and small businesses, we've seen the same errors cost people hundreds (sometimes thousands) of dollars every year. Here's what you need to know to maximize your tax refund in 2026.

Mistake #1: Taking the Standard Deduction Without Running the Numbers!

The standard deduction for 2026 is $15,000 for single filers and $30,000 for married couples filing jointly. That sounds good, right? Here's the problem: you might qualify for more by itemizing.

Most taxpayers automatically take the standard deduction because it's easier. But with the 2026 SALT (state and local tax) cap increasing, itemizing could save you significantly more money.

How to fix it:

- Write down ALL tax-deductible expenses: mortgage interest, property taxes, state income taxes, charitable donations, and medical costs exceeding 7.5% of your income

- Add them up and compare to the standard deduction

- Use IRS Schedule A to itemize if your total exceeds the standard amount

If you own a home in New Haven or made substantial charitable contributions, itemizing is worth the extra paperwork. A concierge tax pro can run both scenarios in minutes to find your best option.

Mistake #2: Missing New 2026 Deductions You Qualify For!

The 2026 tax code introduced several new deductions that many taxpayers don't know exist. If you're not claiming them, you're literally giving money back to the government.

New deductions for 2026 include:

- Overtime Pay Deduction: Allows exclusion of certain overtime earnings from taxable income

- Tips Deduction: Service industry workers can deduct a portion of tip income

- Vehicle Interest Deduction: Deduct interest on auto loans used for work-related purposes

How to fix it:

- Review your income sources to identify qualifying earnings

- Gather documentation showing overtime hours, tip records, or vehicle loan statements

- Claim these deductions on the appropriate forms when filing

Even small deductions add up. A $500 deduction could save you $100-150 in taxes depending on your bracket.

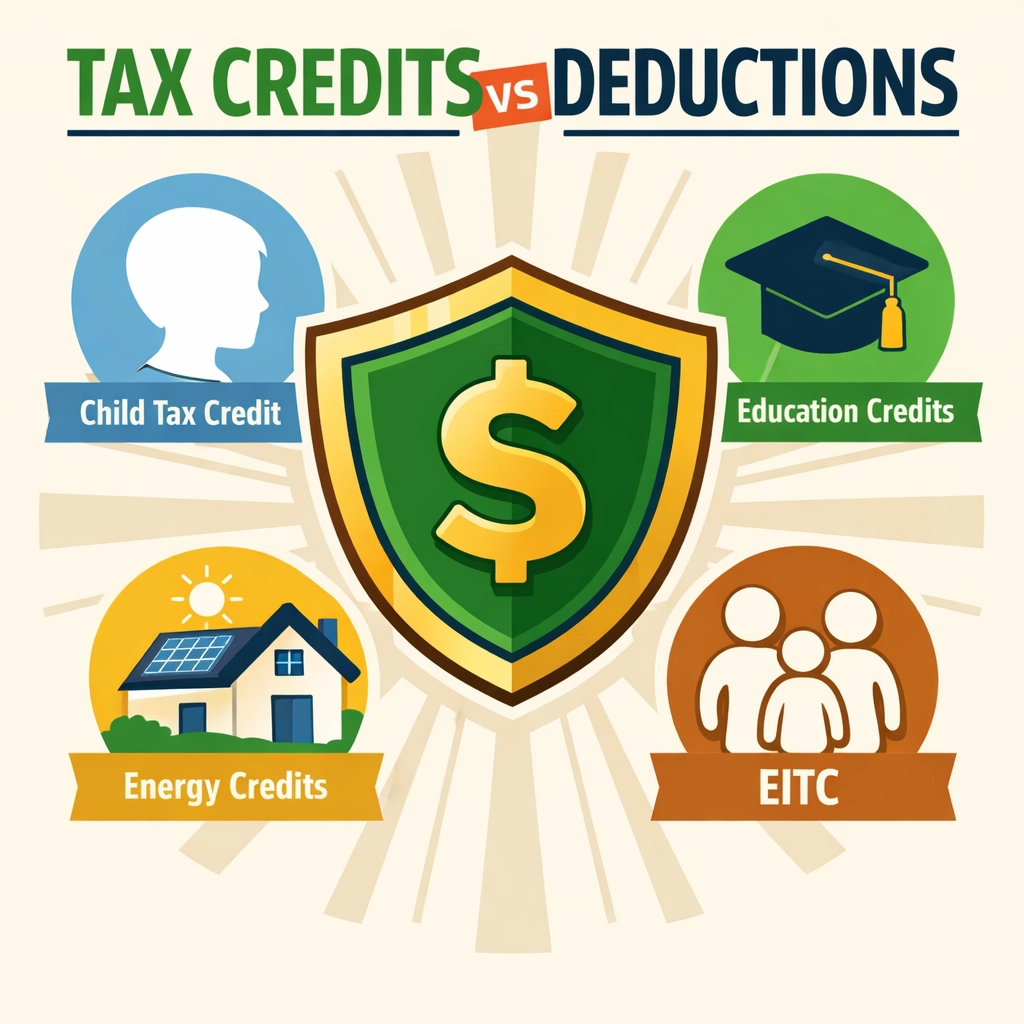

Mistake #3: Ignoring Tax Credits (They're Worth MORE Than Deductions!)

Here's something many people don't understand: tax credits reduce your tax bill dollar-for-dollar, while deductions only reduce your taxable income. Yet millions of eligible Americans fail to claim credits they qualify for.

Major tax credits for 2026:

- Child Tax Credit: Up to $2,000 per qualifying child

- Earned Income Tax Credit: Worth up to $7,830 for families

- American Opportunity Credit: Up to $2,500 for college expenses

- Energy Efficiency Credits: For home improvements like solar panels or heat pumps

How to fix it:

- Check eligibility requirements for each credit

- Gather supporting documents (birth certificates for dependents, tuition statements, contractor invoices)

- Complete the proper forms and worksheets

- Double-check income thresholds: many credits phase out at higher income levels

If you have children, paid for education, or made energy-efficient home improvements, you may be missing thousands in available credits.

Mistake #4: Not Maximizing Retirement Contributions and HSAs!

Pre-tax contributions to retirement accounts reduce your taxable income right now while building your future wealth. Yet countless people contribute less than they could: or nothing at all.

How to fix it:

- Contribute the maximum to your 401(k): $23,500 in 2026 ($31,000 if age 50+)

- Make IRA contributions: Up to $7,000 ($8,000 if age 50+)

- Fund a Health Savings Account (HSA): $4,300 for individuals, $8,550 for families

- Make contributions before the April 15 deadline for the previous tax year

A $5,000 401(k) contribution could save you $1,000-1,500 in taxes depending on your bracket. An HSA offers triple tax benefits: deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses.

Mistake #5: Terrible Record-Keeping (or No Records at All!)

You can't claim deductions you can't prove. The IRS may request documentation for any deduction or credit you claim, and without proper records, you'll lose those benefits: plus potentially face penalties.

How to fix it:

- Create a dedicated folder (physical or digital) for all tax documents

- Save receipts for deductible expenses throughout the year

- Keep bank statements, credit card statements, and canceled checks

- Maintain mileage logs for business or medical travel

- Store documents for at least three years (seven years for more complex situations)

Use smartphone apps to photograph receipts immediately. Cloud storage ensures you won't lose documents in a coffee spill or computer crash.

Mistake #6: Poor Income Timing Strategy!

When you receive income matters just as much as how much you earn. Receiving a large bonus in December could push you into a higher tax bracket unnecessarily.

How to fix it:

- Request year-end bonuses be paid in January if you're near a bracket threshold

- Delay invoicing for freelance work until January if beneficial

- Accelerate deductible expenses into the current year

- Consider Roth IRA conversions in lower-income years

This requires planning ahead. A professional tax preparer in New Haven can model different scenarios to optimize your income timing for 2026 and beyond.

Mistake #7: Ignoring Tax-Loss Harvesting (Investors, This Means You!)

If you have taxable investment accounts, you can use investment losses to offset capital gains and reduce your tax bill. Most investors miss this opportunity entirely.

How to fix it:

- Review your investment portfolio for positions with losses

- Sell losing investments to realize the loss for tax purposes

- Offset capital gains with capital losses

- Deduct up to $3,000 in excess losses against ordinary income annually

- Carry forward additional losses to future tax years

Be aware of the wash-sale rule: you cannot repurchase the same or substantially identical security within 30 days before or after the sale.

Time to Take Action!

The difference between a small refund and a maximum refund often comes down to these seven mistakes. With the new 2026 tax rules, you have more opportunities than ever to reduce your tax bill: but only if you know what to claim and how to claim it correctly.

Your next steps:

- Gather all tax documents and receipts

- Review the seven mistakes above and identify which apply to you

- Calculate whether itemizing beats the standard deduction

- Verify you're claiming all eligible credits and deductions

- Consider working with a tax preparation professional who knows the 2026 rules

At Jose's Tax Service, we specialize in finding every deduction and credit you qualify for. Our concierge tax preparation service means we handle the complex calculations, stay updated on New Haven-specific tax issues, and ensure you get your maximum refund: guaranteed.

Don't leave money on the table this year. File smart, file early, and maximize your 2026 tax refund.

Need help navigating the new 2026 tax rules? Contact Jose's Tax Service for expert tax preparation in New Haven. We'll make sure you're not making these costly mistakes.

Leave a Reply

You must be logged in to post a comment.