Maximize Your Tax Refund in 2026: 7 Mistakes You’re Making (and How to Fix Them)

The IRS expects 2026 to be one of the best refund seasons in years. New tax rules benefit middle-class families, workers with overtime pay, and anyone earning tips. But here's the problem: most taxpayers are leaving money on the table because they're making preventable mistakes.

If you want to maximize your tax refund this year, you need to avoid these seven common errors. Let's fix them right now.

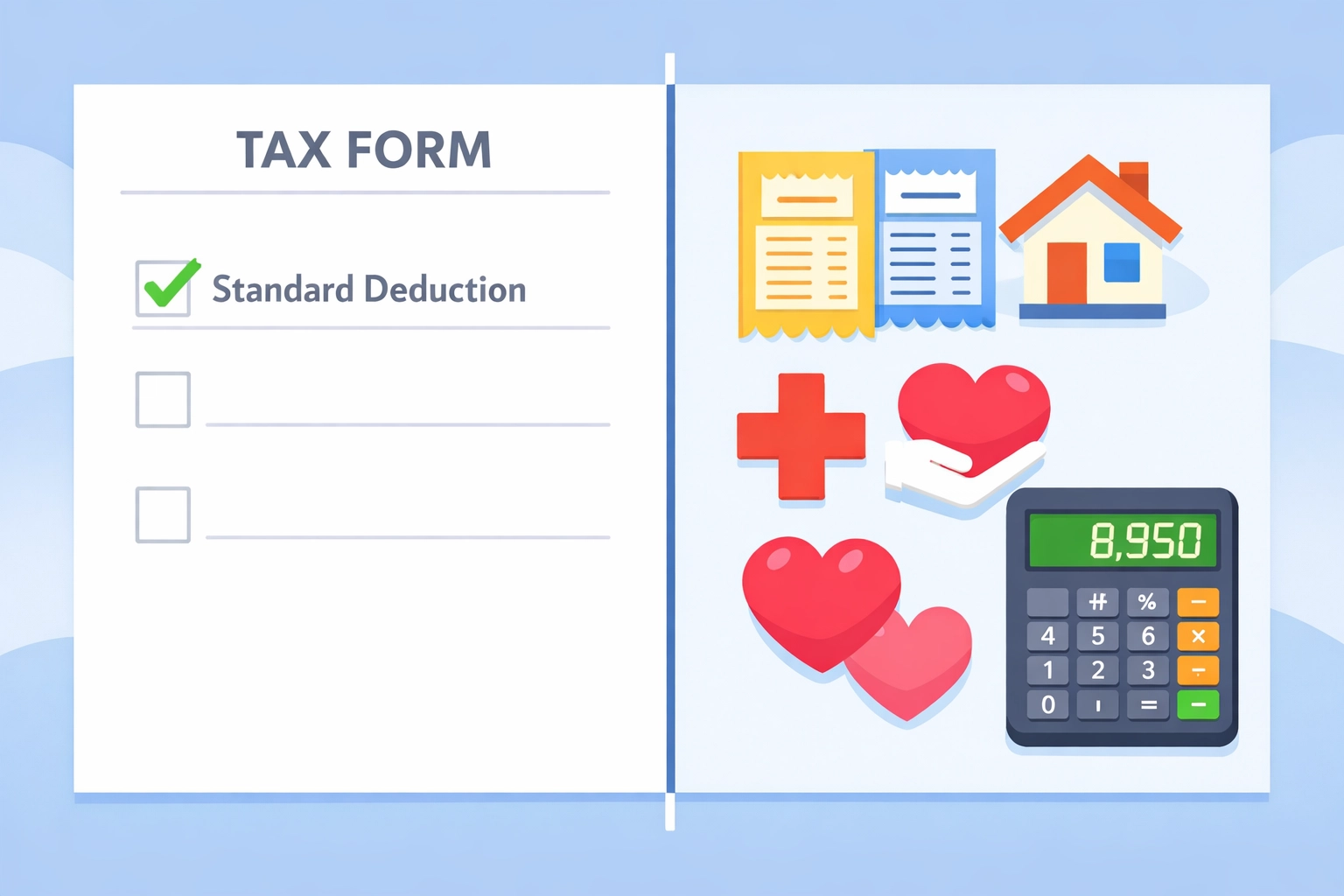

Mistake #1: Taking the Standard Deduction Without Checking if Itemizing Saves You More!

The standard deduction for 2026 is higher than ever. But that doesn't mean it's always your best choice.

Many taxpayers automatically take the standard deduction without calculating whether itemizing would save them more money. With the new SALT (State and Local Tax) cap increase, you can now write off more state and local taxes than before.

Common itemized deductions include:

- State and local taxes (now with a higher cap)

- Mortgage interest on your home loan

- Charitable donations to qualified organizations

- Medical expenses exceeding 7.5% of your adjusted gross income

- Work-related expenses if you're self-employed

How to fix it: Use Schedule A to calculate your itemized deductions. Compare the total to your standard deduction amount. File using whichever method gives you the lower taxable income. A concierge tax pro in New Haven can run both scenarios in minutes and show you exactly which option maximizes your refund.

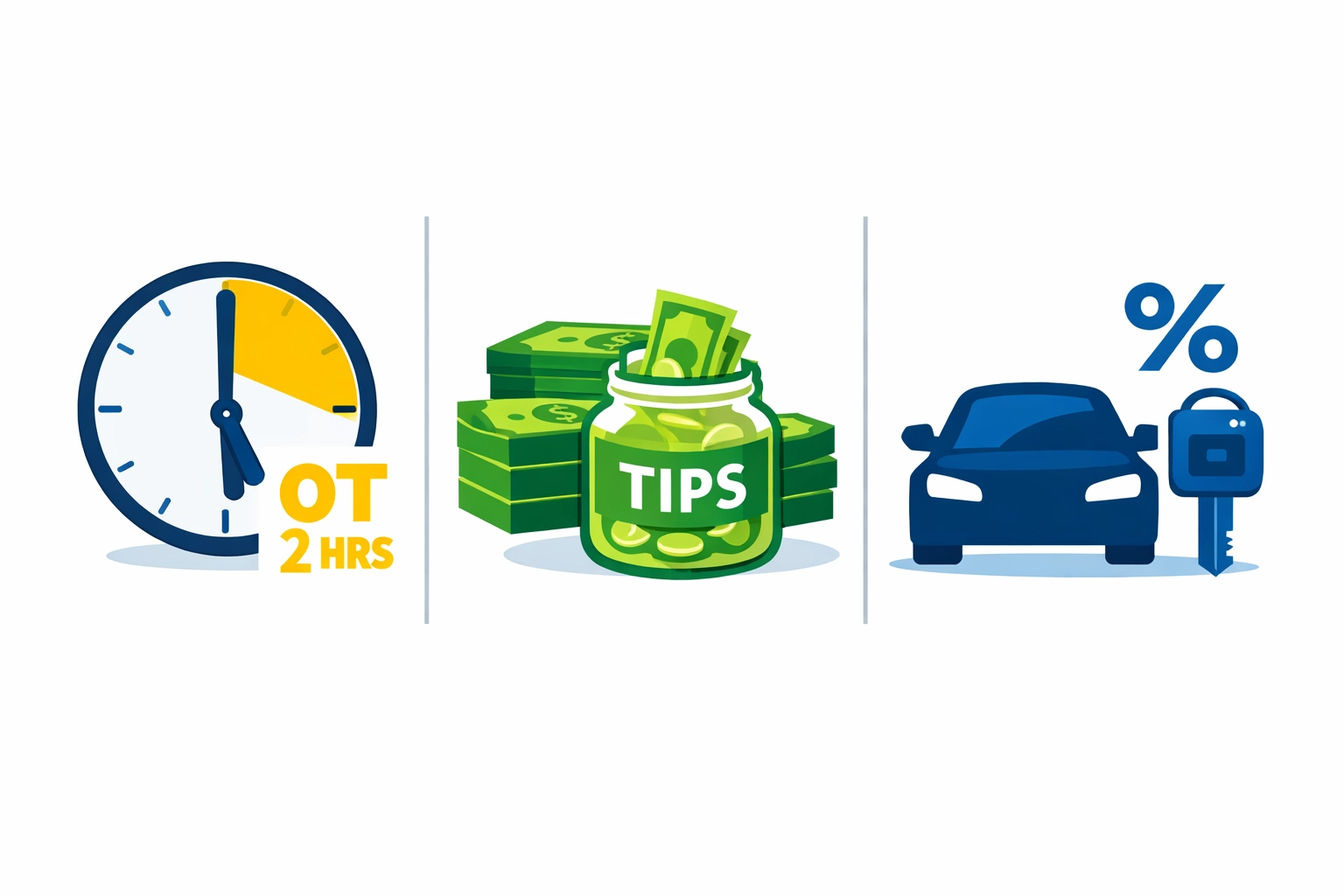

Mistake #2: Missing the New 2026 Deductions That Could Save You Thousands!

2026 introduced several brand-new deductions that didn't exist in previous tax years. Most taxpayers don't even know these exist yet.

Three new deductions you cannot afford to miss:

- Overtime Pay Deduction: Reduce your taxable income by a portion of overtime earnings

- Tips Deduction: Workers in tipping positions can now deduct part of their tips (average tax cut of approximately $1,400 for eligible filers)

- Vehicle Interest Deduction: Write off interest on car loans used for work purposes

How to fix it: Review your pay stubs and identify overtime hours worked. Gather documentation for tips received throughout the year. Collect car loan interest statements if you use your vehicle for business. These deductions require specific documentation, so organize your records now before the April 15 deadline.

Mistake #3: Leaving Tax Credits on the Table!

Tax credits are better than deductions. They reduce your tax bill dollar-for-dollar, not just your taxable income.

The problem? Many taxpayers qualify for credits but never claim them because they don't know the credits exist or they assume they don't qualify.

Available tax credits for 2026 include:

- Child Tax Credit

- Child and Dependent Care Credit

- Earned Income Tax Credit (EITC)

- American Opportunity Credit or Lifetime Learning Credit for education expenses

- Energy efficiency and clean energy credits for home improvements

How to fix it: Review the eligibility requirements for each credit. Don't assume you don't qualify based on income alone: many credits have phase-out ranges that extend higher than you think. Use IRS tools or consult with a tax preparation service in New Haven to identify every credit you're eligible to claim.

Mistake #4: Not Maximizing Retirement Contributions Before December 31st!

Contributions to retirement accounts reduce your taxable income for the year. But most people don't maximize these contributions before the deadline passes.

2026 contribution limits:

- 401(k): Up to $23,000 (plus catch-up contributions if you're 50 or older)

- Traditional IRA: Up to $7,000 (plus catch-up contributions)

- Health Savings Account (HSA): Available limits based on coverage type

How to fix it: Calculate how much you contributed to retirement accounts in 2026. If you didn't max out, increase contributions for 2027 starting immediately. For HSAs, verify your contribution total and make additional contributions if you haven't reached the limit. Remember: Traditional IRA contributions can be made up until the tax filing deadline for the previous year, giving you extra time to reduce your taxable income.

Mistake #5: Getting Your Withholding Wrong All Year Long!

Many taxpayers receive smaller refunds than expected: or owe money: because their withholding was incorrect throughout the year.

Your withholding should match your actual tax liability. If you're getting a huge refund, you gave the IRS an interest-free loan all year. If you owe money, you may face penalties and interest charges.

How to fix it: Use the IRS Tax Withholding Estimator annually. File a new W-4 form with your employer whenever your income or family situation changes. Life events that require a W-4 update include marriage, divorce, birth of a child, purchasing a home, or starting a side business. Adjust your withholding now to optimize your refund for next year while keeping more money in your paycheck throughout 2027.

Mistake #6: Not Timing Your Income Strategically!

When you receive income matters just as much as how much income you receive.

Strategic income timing can keep you in a lower tax bracket or allow you to claim additional deductions in high-income years.

Strategic timing techniques include:

- Delaying year-end bonuses to January if you're close to a higher tax bracket

- Accelerating freelance or consulting payments into December if you have deductions to offset the income

- Bunching charitable donations into one year instead of spreading them across multiple years

- Selling investments strategically to offset gains with losses (tax-loss harvesting)

How to fix it: Review your projected income for the final months of the year. Calculate which tax bracket you'll land in. Make strategic decisions about when to receive payments based on your overall tax situation. If you sell investments, offset capital gains with investment losses. You can use up to $3,000 of losses to offset ordinary income annually, with unused losses carried forward to future years.

Mistake #7: Keeping Terrible Records Throughout the Year!

Poor record-keeping is the number one reason taxpayers miss deductions and credits they're entitled to claim.

Without proper documentation, you can't prove your expenses to the IRS. Without proof, you can't claim the deduction: even if you legitimately incurred the expense.

Essential records to maintain:

- Receipts for all deductible expenses

- Bank statements showing payments

- Mileage logs for business use of your vehicle

- Form 1099s from all income sources

- W-2 forms from employers

- Form 1098 for mortgage interest

- Charitable donation receipts with organization details

How to fix it: Create a dedicated folder (physical or digital) for tax documents. File receipts immediately when you receive them. Use apps or spreadsheets to track deductible expenses in real-time. Keep records for at least three years after filing your return (the IRS can audit returns filed within the past three years). If you claimed a large deduction or credit, keep records for seven years.

What Professional Tax Preparation in New Haven Can Do for You

These seven mistakes cost taxpayers thousands of dollars every year. But here's the good news: they're all fixable with proper planning and expert guidance.

A concierge tax pro doesn't just prepare your return: they actively look for deductions and credits you qualify for, apply the new 2026 rules correctly, and structure your tax situation to maximize your refund while minimizing your liability.

Professional tax preparation means you don't have to become a tax expert yourself. You get personalized attention, strategic year-round planning, and the confidence that your return is accurate and optimized.

Ready to maximize your tax refund? Don't let these mistakes cost you money in 2026. Strategic planning and expert guidance can make this your best refund year yet. Visit Jose's Tax Service to schedule your consultation and discover exactly how much more you could be getting back.

Leave a Reply

You must be logged in to post a comment.