How to Maximize Your Tax Refund in 2026: The Year-Round Planning Secret

New Haven, CT : February 13, 2026 : Most taxpayers approach tax season as a once-a-year event, but this strategy leaves money on the table. Strategic year-round tax planning can increase your 2026 refund by thousands of dollars through deliberate timing of income, maximized deductions, and proper utilization of tax-advantaged accounts.

The 2026 tax year introduced significant changes that benefit New Haven taxpayers who act now rather than wait until April. Understanding these provisions and implementing specific strategies today will position you to maximize your tax refund when filing season arrives.

Why Year-Round Planning Outperforms Last-Minute Filing!

Tax preparation conducted exclusively in March and April limits your options. Deductions must be claimed in the year expenses occurred. Retirement contributions have specific deadlines. Income timing decisions cannot be reversed after December 31.

A proactive approach allows you to:

- Adjust withholdings throughout the year to optimize cash flow

- Time major purchases and expenses for maximum tax benefit

- Monitor income levels to stay within favorable tax brackets

- Make strategic retirement contributions before cutoff dates

- Document deductible expenses as they occur rather than reconstructing records months later

This systematic method can result in refunds 15-30% larger than reactive filing approaches, according to IRS data analysis of comparable taxpayer profiles.

Strategy #1: Maximize Tax-Advantaged Account Contributions

Traditional 401(k)s and Individual Retirement Accounts (IRAs) provide the most powerful refund-boosting mechanism available to wage earners. Contributions directly reduce your taxable income, lowering your overall tax liability dollar-for-dollar within your marginal tax bracket.

Traditional IRA contributions for the 2025 tax year can be made through April 15, 2026. This extended deadline means you can still reduce your 2025 taxable income by up to $7,000 ($8,000 if age 50 or older) by making an IRA contribution before the filing deadline.

Health Savings Accounts (HSAs) offer triple tax advantages:

- Contributions reduce your adjusted gross income

- Funds grow tax-free

- Withdrawals for qualified medical expenses incur no tax

For 2026, HSA contribution limits are $4,300 for individual coverage and $8,550 for family coverage, with an additional $1,000 catch-up contribution allowed for individuals age 55 and older.

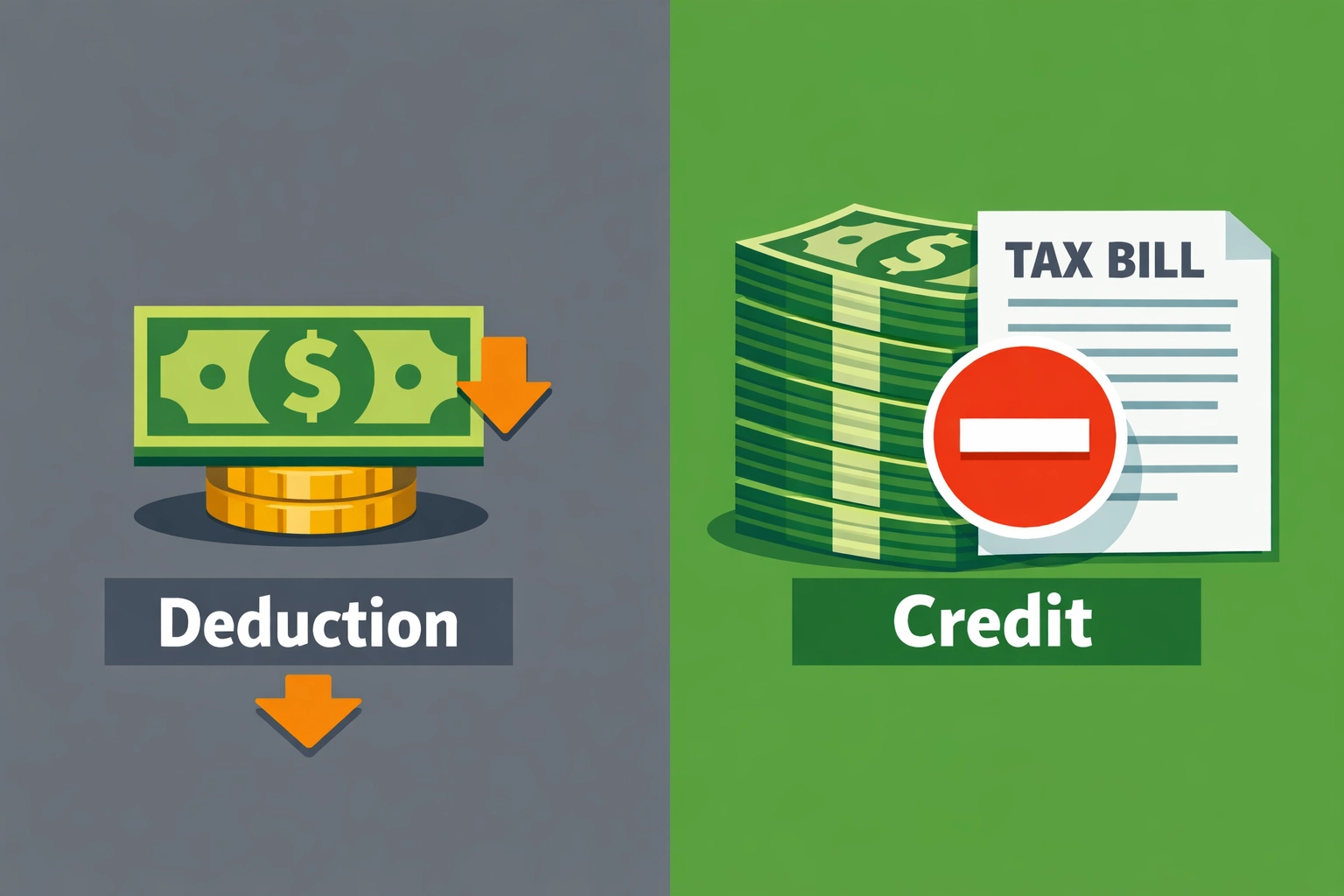

Strategy #2: Prioritize Tax Credits Over Deductions

Tax credits reduce your tax bill dollar-for-dollar, making them substantially more valuable than deductions, which only reduce your taxable income. Understanding this distinction is critical to maximize your tax refund.

High-Impact Tax Credits for 2026:

- Earned Income Tax Credit (EITC): Up to $8,231 for qualifying taxpayers with three or more children

- Child Tax Credit: $2,200 per qualifying child under age 17

- American Opportunity Credit: $2,500 per eligible student for qualified education expenses

- Lifetime Learning Credit: Up to $2,000 for post-secondary education costs

- Child and Dependent Care Credit: Up to $3,000 for one dependent or $6,000 for two or more dependents

Verify your eligibility for each credit. Many New Haven families overlook the Lifetime Learning Credit because they assume education credits only apply to traditional four-year degree programs, but qualifying expenses include vocational schools, professional development courses, and skills training programs.

Strategy #3: Leverage the Expanded SALT Deduction Cap

The 2026 tax law increased the state and local tax (SALT) deduction cap to $40,400 for most filing statuses, representing a significant expansion from previous limits. This provision particularly benefits New Haven taxpayers in Connecticut, where state income taxes and property taxes run higher than the national average.

To maximize this deduction:

- Calculate your total state income tax paid or withheld

- Add your property tax payments

- Include vehicle registration fees (if based on value)

- Consider prepaying January 2027 property taxes in December 2026 if beneficial

Compare your total itemized deductions against the standard deduction ($15,000 for single filers, $30,000 for married filing jointly in 2026). If itemizing produces a larger total, you will reduce your taxable income more substantially.

Strategy #4: Implement the Bunching Strategy

If your deductible expenses typically fall just below the standard deduction threshold, accelerate expenses into a single tax year to exceed it, then claim the standard deduction in alternate years.

This technique works effectively for:

- Charitable contributions (bunch two years of donations into one)

- Medical expenses exceeding 7.5% of your adjusted gross income

- State tax payments (where applicable and beneficial)

- Mortgage interest prepayments

For example, if you normally donate $8,000 annually to charity and have $10,000 in other itemized deductions ($18,000 total), you fall below the married filing jointly standard deduction. By donating $16,000 in one year and $0 the next, you exceed the threshold in year one and claim the standard deduction in year two, resulting in greater cumulative tax savings.

Strategy #5: Time Your Income Strategically

Income timing can keep you in a lower tax bracket or preserve eligibility for income-based credits and deductions. This strategy requires careful planning but delivers substantial results.

Consider these timing tactics:

- Delay year-end bonuses into January if they would push you into a higher bracket

- Accelerate deductible business expenses into December to reduce current-year income

- Time Roth IRA conversions for years when your income is temporarily lower

- Defer freelance or consulting invoice payments until the following year when strategic

Review your projected annual income by November. If you are close to a bracket threshold, implement income deferral or acceleration strategies immediately. Self-employed New Haven professionals and small business owners have the most flexibility with these timing decisions.

New 2026 Tax Provisions You Should Know!

Several new tax provisions took effect for the 2026 tax year. Understanding these changes can increase your refund substantially.

Tip Income Exclusions: Qualifying tipped employees in the food service, hospitality, and personal service industries may exclude a portion of tip income from taxation under specific conditions. If you work in New Haven's restaurant or service sector, verify your eligibility with a tax professional.

Enhanced Small Business Deductions: Business owners can deduct a wider range of marketing and advertising expenses, including digital advertising, website development costs, and social media marketing campaigns. Track these expenses throughout the year for tax preparation purposes.

Energy Efficiency Credits: Residential energy credits have been expanded to include additional qualifying improvements. If you upgraded your New Haven home with energy-efficient windows, insulation, or HVAC systems, you may qualify for credits up to $1,200.

Practical Steps to Implement Today

Taking action now: in February 2026: positions you for maximum refund potential when filing your 2025 return and sets the foundation for optimizing your 2026 tax year.

Immediate Actions:

- Make final 2025 IRA contributions before April 15, 2026 to reduce your 2025 taxable income

- Organize receipts and documentation for all 2025 deductions and credits

- Review your 2026 withholding to ensure proper tax amounts are being withheld throughout the year

- Open an HSA if you have a qualifying high-deductible health plan

- Document business and work-related expenses monthly rather than reconstructing them later

- Schedule a mid-year tax projection with a concierge tax pro to identify planning opportunities

Why Concierge Tax Preparation Maximizes Your Refund

DIY tax software follows algorithmic decision trees that may miss deductions and credits specific to your situation. A concierge tax pro asks probing questions, identifies overlooked deductions, and implements strategic planning throughout the year rather than simply processing forms.

Jose's Tax Service specializes in tax preparation New Haven families and business owners trust for comprehensive, personalized guidance. Our year-round advisory approach identifies every available deduction and credit while ensuring full compliance with current tax law.

Working with an experienced tax professional typically increases refunds by $800-$2,400 compared to self-prepared returns, according to National Association of Tax Professionals research data. This return on investment makes professional preparation financially advantageous for most taxpayers.

Don't Leave Money on the Table!

Maximizing your 2026 tax refund requires strategic action throughout the year, not reactive filing in April. Implement these strategies now to reduce your tax liability, increase your refund, and retain more of your hard-earned income.

The difference between a standard refund and an optimized refund often totals thousands of dollars: money that belongs in your pocket, not left unclaimed due to missed deductions or poor planning.

Schedule a consultation with Jose's Tax Service to develop your personalized year-round tax strategy. Visit josestaxservice.com or contact our New Haven office today to get started. Your maximum refund is waiting: but only if you take action now.

Tags: news, tax planning

Leave a Reply

You must be logged in to post a comment.