7 Mistakes You're Making with Tax Planning in 2026 (And How to Fix Them Before April)

New Haven, CT : February 9, 2026

Tax season is here, and you've got just over two months before the April 15 deadline. If you're still using last year's tax strategy: or worse, no strategy at all: you're setting yourself up for a smaller refund, penalties, or an unwelcome surprise bill from the IRS.

At Jose's Tax Service, we see the same mistakes every single year. The good news? Most of them are fixable right now, before you file. Here are the seven biggest tax planning errors Connecticut taxpayers are making in 2026: and exactly how to correct them before time runs out.

Mistake #1: Missing or Underpaying Your Quarterly Estimated Taxes

If you're self-employed, a freelancer, or a small business owner in New Haven, you're required to pay estimated taxes quarterly. Yet this remains one of the most common: and most expensive: errors we see.

Why it matters: The IRS expects you to pay as you earn. If you wait until April to settle up, you'll face underpayment penalties and interest charges that can add hundreds or even thousands of dollars to your tax bill.

How to fix it now: Review your 2026 income so far. Calculate what you owe for Q1 (due April 15). If your revenue increased significantly in January or February, adjust your payment upward to cover federal income tax and self-employment tax. Don't forget Connecticut state estimated taxes: these are separate and also due quarterly.

Not sure how much to pay? A tax preparer can run a mid-year projection and tell you exactly what to send in to stay compliant and avoid penalties.

Mistake #2: Keeping Messy or Incomplete Records

Disorganized bookkeeping is costing you money. When your receipts are scattered, your personal and business transactions are mixed, and you can't prove your expenses, the IRS won't give you the benefit of the doubt.

Why it matters: Poor record-keeping increases your audit risk and guarantees you'll miss deductions. If you can't substantiate a business expense with proper documentation, you lose that write-off: plain and simple.

How to fix it now: Before April, reconcile all your business bank accounts and credit cards. Separate personal expenses from business expenses completely. Categorize every transaction consistently (office supplies, fuel, meals, etc.). If you've been mixing funds in one account, open a dedicated business checking account immediately.

Consider using bookkeeping software or hiring a professional to clean up your books. Good records directly reduce your taxable income and protect you during an audit.

Mistake #3: Overlooking New 2026 Tax Credits and Deductions

Tax laws change every year, but most people file the same way they always have. That means you're probably missing credits and deductions you're now eligible for: or claiming ones that no longer exist.

Why it matters: Tax credits reduce your bill dollar-for-dollar. Deductions lower your taxable income. Either way, ignoring new opportunities means overpaying the IRS.

How to fix it now: Schedule a consultation with a tax professional before April to review what's changed for 2026. Did you have a child? Start a side business? Make energy-efficient home improvements? Contribute to charity? Each of these could unlock significant tax breaks you didn't qualify for last year.

For Connecticut residents, don't forget state-specific credits like the property tax credit or earned income tax credit (EITC), which can add up to real money back in your pocket.

Mistake #4: Setting Your W-4 Withholding Incorrectly

If your tax withholding is wrong, you're either giving the government an interest-free loan all year (too much withheld) or building a debt you'll have to pay in April (too little withheld).

Why it matters: An incorrect Form W-4 means your employer isn't sending the right amount to the IRS each paycheck. If you under-withhold, you'll owe a balance: possibly with penalties. If you over-withhold, you're missing out on cash flow you could be using throughout the year.

How to fix it now: Review your W-4 immediately if any of these apply to you:

- You started a new job in 2025 or 2026

- Your spouse's income changed

- You got married, divorced, or had a child

- You're working multiple jobs

- You received a large refund or owed a large balance last year

Use the IRS withholding estimator tool to calculate the correct amount, then submit an updated W-4 to your employer. This adjustment will take effect within one to two pay periods and help you avoid surprises in April.

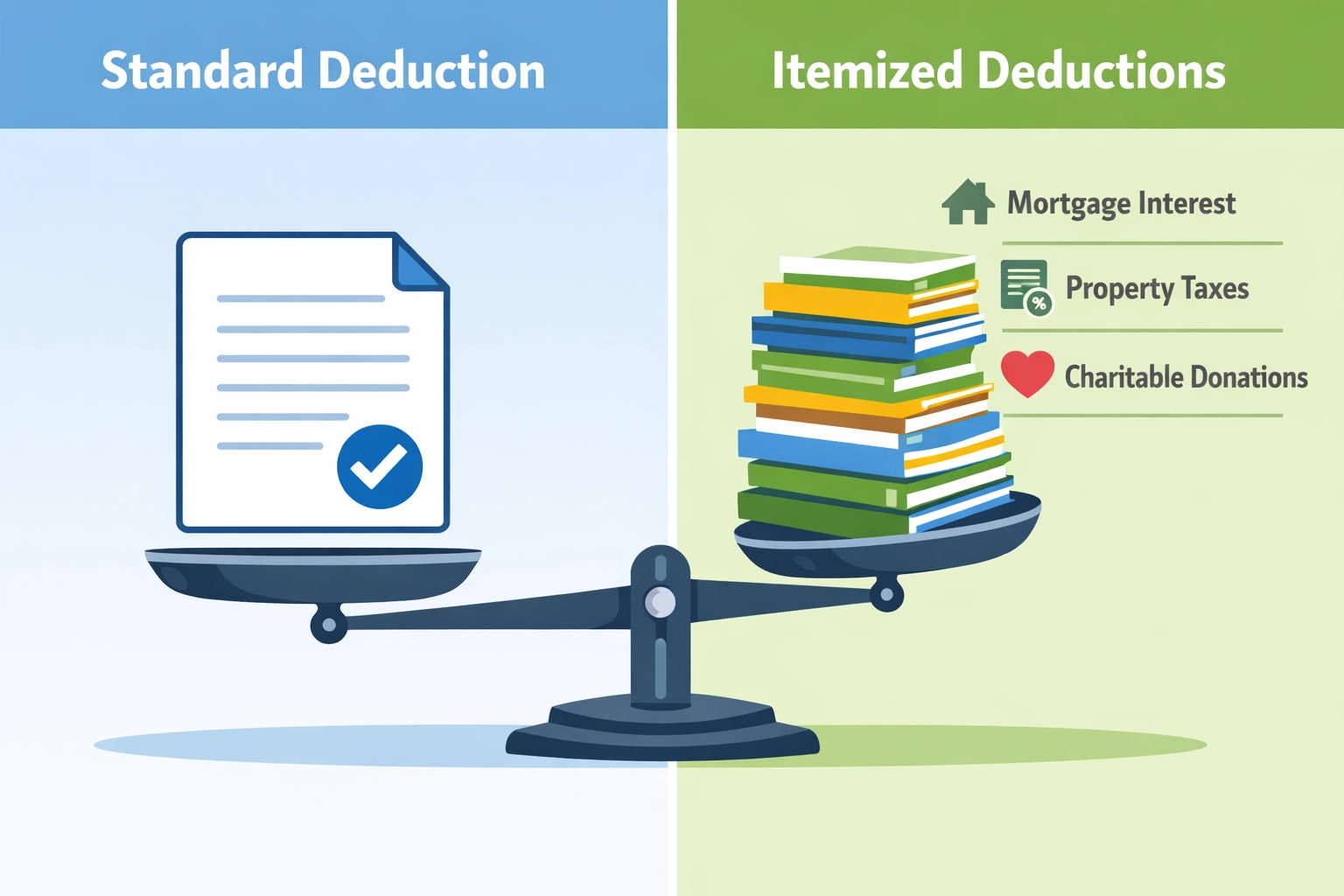

Mistake #5: Claiming the Standard Deduction When Itemizing Makes More Sense

About 90% of taxpayers take the standard deduction because it's easier. But "easier" doesn't mean "better" for your wallet.

Why it matters: For 2026, the standard deduction is $14,600 for single filers and $29,200 for married couples filing jointly. But if you have significant mortgage interest, property taxes, state income taxes, or charitable contributions, itemizing could save you substantially more.

Here's the big change for 2026: Under recent tax legislation, the SALT (state and local tax) deduction cap has increased to $40,000: up from the previous $10,000 limit. If you're a Connecticut homeowner paying high property taxes or state income taxes, this change is a game-changer.

How to fix it now: Add up your itemizable deductions:

- Mortgage interest

- Connecticut property taxes

- State income taxes paid

- Charitable contributions

- Medical expenses exceeding 7.5% of your income

If your total exceeds the standard deduction, itemize. If you're close, a few strategic charitable donations before April could push you over the threshold. A tax preparer can run both scenarios and show you which saves more money.

Mistake #6: Not Maximizing Tax-Advantaged Retirement Accounts

Failing to use tax-advantaged accounts like 401(k)s, traditional IRAs, and HSAs means you're paying more tax than necessary: and saving less for your future.

Why it matters: Contributions to these accounts reduce your taxable income directly. Every dollar you contribute lowers your tax bill for 2026 while building your retirement savings.

How to fix it now: Increase your 401(k) contributions before April if possible. For 2026, you can contribute up to $23,000 to a 401(k) if you're under 50, or $30,500 if you're 50 or older.

If you're eligible for a traditional IRA, you have until April 15, 2027 to make contributions that count for the 2026 tax year. The limit is $7,000 ($8,000 if you're 50+).

Don't forget Health Savings Accounts (HSAs). If you have a high-deductible health plan, HSA contributions are triple-tax-advantaged: deductible going in, grow tax-free, and come out tax-free for medical expenses.

If you're self-employed, ask your tax preparer about SEP IRAs or Solo 401(k)s: these allow much higher contribution limits and can dramatically reduce your 2026 tax bill.

Mistake #7: Ignoring Connecticut State and Local Tax Obligations

Federal taxes get all the attention, but your Connecticut state return is just as important: and just as complicated.

Why it matters: Connecticut has its own credits, deductions, and tax rates that don't match federal rules. Missing state-level breaks is one of the easiest ways to overpay, especially with Connecticut's higher-than-average tax rates.

How to fix it now: Review Connecticut-specific opportunities before you file:

- Property tax credit: Available to Connecticut homeowners and renters

- Earned Income Tax Credit (EITC): Connecticut offers a state-level credit worth up to 30.5% of your federal EITC

- College savings deduction: Contributions to a Connecticut Higher Education Trust (CHET) account are deductible

- Pass-through entity tax (PTET): If you own a business structured as an S corporation or partnership, Connecticut's PTET election could save you significant money by working around the SALT cap

If you work remotely for an out-of-state employer or earned income in multiple states, you may need to file returns in more than one state. Get this wrong and you could be double-taxed or face penalties for not filing where required.

Take Action Before April 15

You have two months to fix these mistakes and maximize your tax refund for 2026. The longer you wait, the fewer options you'll have.

At Jose's Tax Service, we specialize in tax preparation for New Haven residents and small business owners. We'll review your situation, identify missed opportunities, and file your return accurately and on time.

Don't leave money on the table. Schedule your appointment today and let's make sure you're paying the IRS exactly what you owe: nothing more.

Categories: News, Tax Planning

Keywords: tax planning, tax update, tax preparation new haven, maximize tax refund

Leave a Reply

You must be logged in to post a comment.