Self-Employed? How to Manage Quarterly Estimated Taxes and Avoid Costly Penalties

NEW HAVEN, CT – February 5, 2026 – Self-employed individuals and small business owners face a critical responsibility that traditional W-2 employees never encounter: quarterly estimated tax payments. Miss a deadline or underpay, and you'll face penalties that can add hundreds: or even thousands: of dollars to your tax bill.

Understanding how to calculate and manage these payments is essential for avoiding costly mistakes. Here's what every self-employed professional in New Haven needs to know about quarterly estimated taxes.

Why Quarterly Estimated Taxes Matter!

The U.S. tax system operates on a pay-as-you-go basis. When you work for an employer, taxes are withheld from each paycheck automatically. But when you're self-employed: whether you're a freelancer, consultant, independent contractor, or small business owner: you must proactively pay estimated taxes throughout the year.

These payments cover three primary tax obligations:

- Federal income tax based on your taxable income

- Self-employment tax (15.3% on net self-employment income up to $176,100 for 2026; 2.9% above that threshold)

- Additional Medicare tax (0.9% on self-employment income exceeding $200,000 for single filers or $250,000 for married couples filing jointly)

The IRS requires quarterly estimated payments if you expect to owe more than $1,000 in taxes after accounting for withholding and credits.

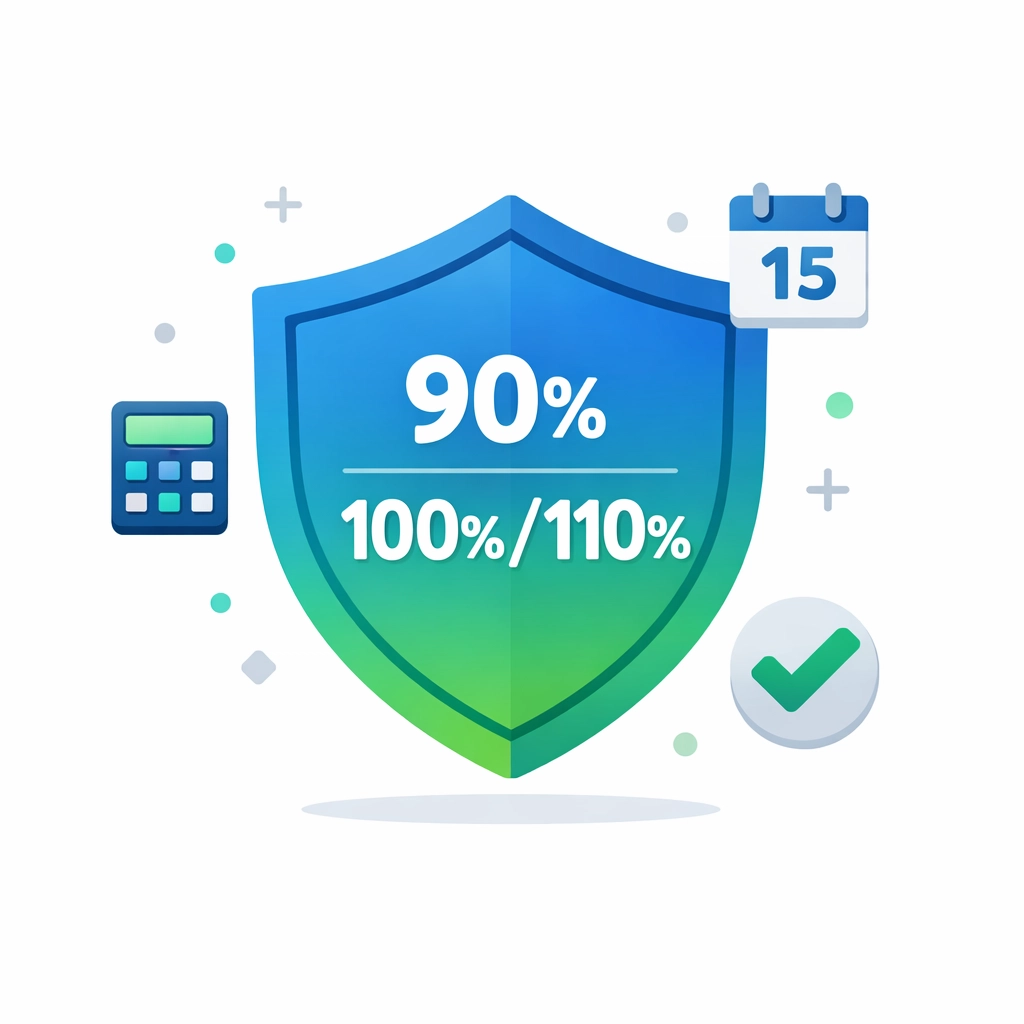

Safe Harbor Rules: Your Protection Against Penalties!

The IRS provides clear safe harbor guidelines that protect you from underpayment penalties. Meet either of these requirements, and you're in the clear: even if you owe additional tax when filing your annual return:

Option 1: Pay 90% of Your Current Year's Tax

Calculate your estimated tax liability for 2026 and pay at least 90% of that amount through quarterly installments.

Option 2: Pay 100% of Your Prior Year's Tax (110% for High Earners)

If your 2025 adjusted gross income (AGI) was $150,000 or less ($75,000 if married filing separately), pay 100% of your 2025 tax liability divided into four quarterly payments. If your AGI exceeded those thresholds, you must pay 110% of your prior year's tax.

This second option is often simpler because you already know last year's total tax liability. You don't need to estimate current-year income, which can fluctuate significantly for self-employed individuals.

Two Methods for Calculating Quarterly Payments!

Method 1: Prior-Year Method (Simplest Approach)

Take your total tax liability from your 2025 tax return (found on Form 1040, line 24). Divide that number by four.

Example: If you owed $24,000 in total tax for 2025, and your AGI was under $150,000, you'd pay $6,000 per quarter in 2026 ($24,000 ÷ 4 = $6,000).

If your 2025 AGI exceeded $150,000, multiply your tax liability by 1.10 first, then divide by four. Using the same example: $24,000 × 1.10 = $26,400 ÷ 4 = $6,600 per quarter.

This method provides certainty and simplicity. The downside? If your income drops significantly in 2026, you may overpay. If it increases substantially, you'll owe more when you file.

Method 2: Annualized Income Method (More Precise)

This approach requires more record-keeping but offers greater accuracy, especially if your income varies throughout the year. Calculate your actual income and expenses for each quarter, then annualize that figure to estimate your full-year tax obligation.

Basic calculation steps:

- Estimate your total annual self-employment income

- Subtract business expenses and the standard deduction ($16,100 for single filers in 2026; $32,200 for married filing jointly)

- Apply IRS tax brackets to your taxable income

- Add self-employment tax (15.3% on net earnings up to $176,100; 2.9% above that)

- Add Additional Medicare tax if applicable (0.9% above income thresholds)

- Divide the total by four

Use IRS Form 1040-ES as your guide. This form includes a comprehensive worksheet that walks you through the calculation process step by step.

2026 Quarterly Payment Deadlines: Don't Miss These!

Mark these dates on your calendar. Late payments trigger penalties calculated from the due date until the payment date:

- 1st Quarter (January 1 – March 31): April 15, 2026

- 2nd Quarter (April 1 – May 31): June 16, 2026

- 3rd Quarter (June 1 – August 31): September 15, 2026

- 4th Quarter (September 1 – December 31): January 15, 2027

Note that the second and third quarters are not exactly three months long. The IRS sets these specific deadlines, and they don't always align with calendar quarters.

Practical Strategies for Managing Estimated Taxes!

Track Income and Expenses Quarterly

Don't wait until year-end to organize your finances. Review your profit and loss statement every three months. This quarterly discipline makes accurate tax estimates easier and helps you adjust payments if your income changes significantly mid-year.

Implement the 30% Rule

Many tax professionals recommend setting aside 30% of every payment you receive from clients. Transfer this amount immediately to a separate savings account designated for taxes. This percentage typically covers federal income tax, self-employment tax, and state taxes (if applicable in your location).

Adjust Withholding If You Also Have W-2 Income

If you have both self-employment income and employment income, consider asking your employer to increase withholding from your paycheck. Complete a new Form W-4 to adjust your withholding. This strategy may eliminate the need for separate quarterly estimated payments.

Make Adjustments When Income Changes

Your income can fluctuate throughout the year. If you land a major contract in Q3, increase your remaining quarterly payments to avoid underpayment penalties. If business slows down, you can reduce subsequent payments.

Use Electronic Payment Methods

The IRS offers several convenient payment options:

- IRS Direct Pay (free, directly from your bank account)

- Electronic Federal Tax Payment System (EFTPS) (free, requires enrollment)

- Credit or debit card (convenience fees apply)

- Same-day wire transfer (for emergency situations)

Electronic payments provide immediate confirmation and eliminate the risk of lost checks.

When Professional Help Makes Sense!

Calculating estimated taxes accurately requires understanding complex tax code provisions, deduction rules, and quarterly adjustments. Many self-employed individuals benefit from professional guidance, especially in their first year of self-employment or when experiencing significant income changes.

Jose's Tax Service specializes in helping New Haven-area self-employed professionals and small business owners navigate quarterly estimated tax requirements. With expertise in tax planning and preparation, we ensure you pay the right amount at the right time: avoiding both underpayment penalties and unnecessary overpayment.

Our $0 upfront payment options make professional tax assistance accessible when you need it most. We'll review your income, calculate accurate quarterly payments, and provide ongoing guidance throughout the year.

The Bottom Line!

Managing quarterly estimated taxes doesn't have to be overwhelming. Choose the calculation method that works best for your situation: prior-year method for simplicity or annualized income method for precision. Make payments on time. Set aside money consistently. And don't hesitate to seek professional help when needed.

The penalty for underpayment can reach 8% annually on the underpaid amount, calculated from the due date until you pay. That's an expensive mistake when proper planning can prevent it entirely.

Take control of your quarterly tax obligations now. Your future self: and your bank account: will thank you.

Need help calculating your 2026 quarterly estimated taxes? Contact Jose's Tax Service today at josestaxservice.com to schedule a consultation. Let's create a tax payment strategy that protects you from penalties while optimizing your cash flow throughout the year.

Leave a Reply

You must be logged in to post a comment.