7 Mistakes You're Making with the New 2026 Tax Deductions (And How to Fix Them)

Tax season 2026 brought significant changes to deductions, and most taxpayers are getting them wrong. The IRS rolled out new rules that impact everything from charitable giving to dependent care, and if you're not paying attention, you're leaving money on the table.

Here at Jose's Tax Service in New Haven, we've already spotted these mistakes dozens of times this season. The good news? They're all fixable. Let's break down the seven most common errors people are making with 2026 deductions and show you exactly how to correct them.

Mistake #1: Missing the New Non-Itemizer Charitable Deduction!

The Problem: You donated to charity but didn't claim the deduction because you take the standard deduction.

For the first time in years, the IRS reinstated a special charitable deduction for people who don't itemize. You can now deduct up to $1,000 in cash charitable contributions ($2,000 for married filing jointly) even while claiming the standard deduction.

Most taxpayers assume charitable deductions only work if you itemize. That's no longer true in 2026.

How to Fix It:

- Gather receipts for all cash donations made to qualified charitable organizations in 2025

- Enter these donations on Form 1040, line 12b (the designated non-itemizer charitable line)

- Double-check that your charity is IRS-qualified using the Tax Exempt Organization Search tool

- Keep written acknowledgment from the charity for any single donation over $250

This deduction is above-the-line, meaning it reduces your adjusted gross income (AGI). Don't skip it.

Mistake #2: Ignoring the 0.5% AGI Threshold for Itemized Charitable Gifts!

The Problem: You itemize deductions but didn't realize charitable gifts now require a minimum threshold.

Here's where it gets tricky. If you do itemize, the IRS added a new rule: charitable contributions must exceed 0.5% of your adjusted gross income before you can claim any deduction.

Example: Your AGI is $100,000. You donated $400 to charity. Since $400 is less than $500 (0.5% of $100,000), you get zero deduction.

How to Fix It:

- Calculate 0.5% of your AGI

- Add up all qualified charitable contributions

- Only deduct the amount that exceeds the threshold

- Consider bunching charitable donations into alternating years to clear the threshold

If you're close to the threshold, strategic planning can save you hundreds. Jose's Tax Service can run projections to determine whether itemizing or taking the standard deduction benefits you more.

Mistake #3: Not Understanding SALT Cap Phase-Outs!

The Problem: You maxed out your state and local tax (SALT) deduction without checking if you're subject to phase-out limits.

The SALT deduction cap increased to $40,400 for 2026 (up from $40,000 in 2025). But high earners face phase-out rules that weren't widely publicized.

The phase-out begins at a modified adjusted gross income (MAGI) of $505,000 and fully eliminates the SALT deduction at $606,333.

How to Fix It:

- Calculate your modified adjusted gross income

- Determine if your income falls within the phase-out range

- Adjust your expected SALT deduction accordingly using the IRS phase-out formula

- Explore tax planning strategies to reduce MAGI if you're near the threshold

Many New Haven residents, especially those in higher tax brackets, assume they'll automatically get the full $40,400 deduction. That assumption can lead to unpleasant surprises when filing.

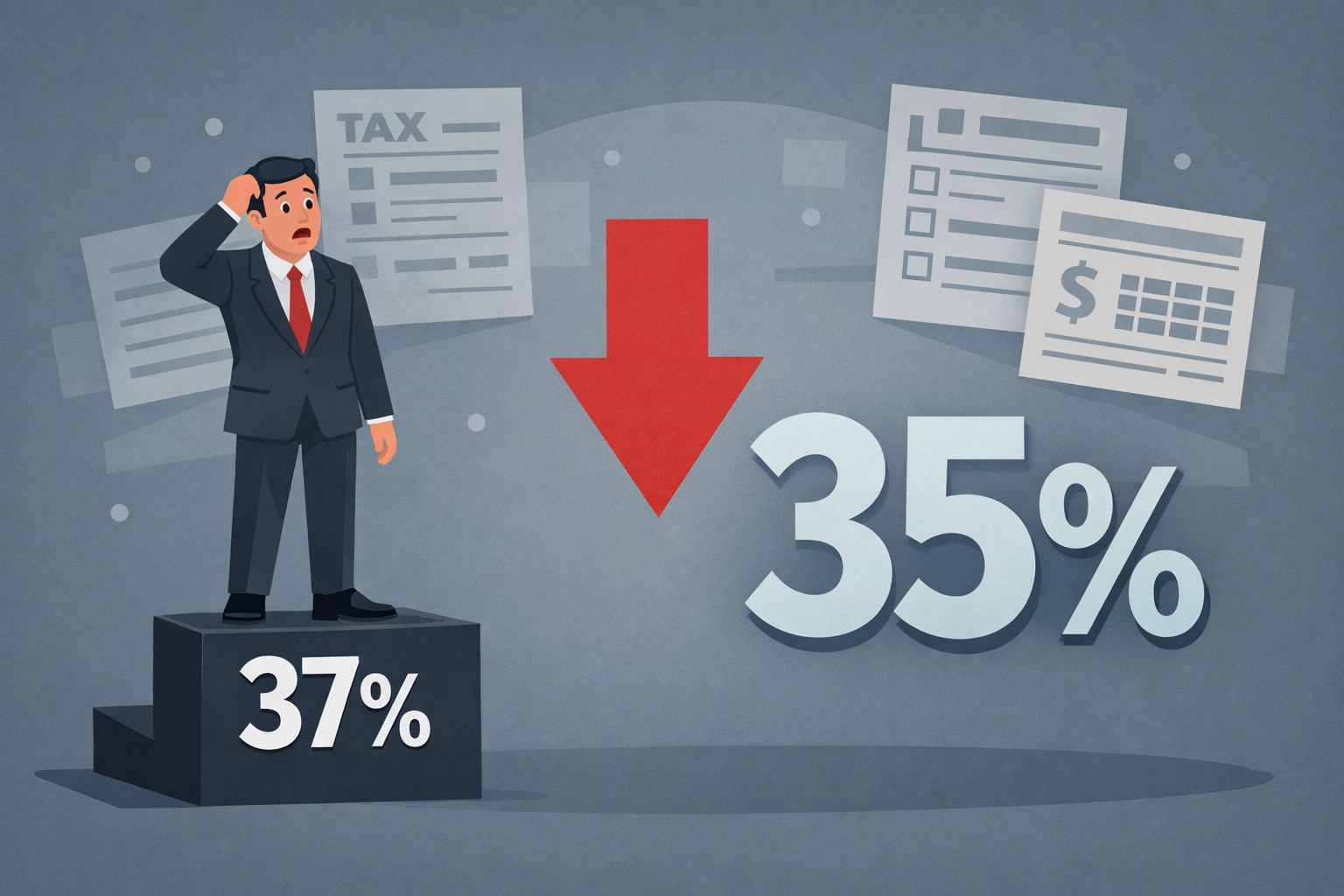

Mistake #4: Overlooking the 37% Bracket Deduction Limitation!

The Problem: You're in the top tax bracket and calculated deductions using the full 37% rate.

Here's a critical change: taxpayers in the 37% tax bracket now only receive a 35% tax benefit from itemized deductions. The IRS effectively capped the benefit rate, reducing the value of every deduction you claim.

This impacts mortgage interest, state taxes, charitable contributions, and medical expenses.

How to Fix It:

- Recalculate the actual tax savings from your itemized deductions using the 35% rate

- Reassess whether itemizing still makes sense compared to the standard deduction

- Consider accelerating or deferring deductible expenses based on expected income changes

- Consult with a tax professional about alternative strategies to maximize your benefit

This limitation catches high earners off guard. If you're in the 37% bracket, your deductions are worth less than you think.

Mistake #5: Forgetting to Maximize Dependent Care FSA Contributions!

The Problem: You contributed the old $5,000 limit to your dependent care flexible spending account (FSA).

The IRS increased the dependent care FSA limit to $7,500 for 2026. If you set your contribution amount in late 2025 based on the old limit, you left $2,500 in potential tax savings on the table.

How to Fix It:

- Contact your employer's benefits administrator immediately

- Request to increase your dependent care FSA contribution to the new $7,500 limit

- Verify the change is reflected in your payroll deductions

- Adjust your budget to account for the higher pre-tax contribution

The $7,500 maximum applies to both married filing jointly and single filers. This is one of the easiest ways to reduce taxable income while covering childcare or elder care expenses.

Mistake #6: Missing the Enhanced Dependent Care Credit!

The Problem: You didn't claim the dependent care credit because you thought your income was too high.

The dependent care tax credit rate increased to 50% of qualifying expenses for 2026 (up from previous years). The credit applies to up to $3,000 in expenses for one dependent or $6,000 for two or more dependents.

Unlike the FSA, which has income limits, the credit is available to more taxpayers than many realize, though the percentage does decrease as income rises.

How to Fix It:

- Calculate your qualifying dependent care expenses

- File Form 2441 (Child and Dependent Care Expenses) with your tax return

- Determine your applicable credit percentage based on your AGI

- Coordinate FSA and credit strategies to maximize total tax benefit

You cannot claim the same expenses for both the FSA and the credit. Strategic planning determines which approach saves you more money. Jose's Tax Service runs these comparisons for every client with dependent care expenses.

Mistake #7: Not Tracking Documentation Properly!

The Problem: You claimed deductions without maintaining proper documentation.

The IRS increased enforcement efforts for the 2026 tax year. Auditors are specifically targeting charitable deductions, home office expenses, and business mileage claims that lack adequate substantiation.

Missing documentation can disallow your entire deduction and may lead to penalties and interest charges.

How to Fix It:

- Maintain receipts for all deductible expenses throughout the year

- Use written acknowledgments from charities for donations over $250

- Keep mileage logs with date, destination, purpose, and miles driven

- Photograph or scan receipts immediately and store them digitally

- Organize documentation by category (medical, charitable, business, etc.)

- Retain records for at least three years after filing

Digital record-keeping tools and apps can automate much of this process. The key is consistency, track expenses as they occur, not at year-end.

Take Action Now!

These seven mistakes are costing New Haven taxpayers thousands of dollars in unclaimed deductions. The 2026 tax law changes created both opportunities and pitfalls, and navigating them requires current knowledge and careful attention to detail.

If you've already filed your 2025 tax return and made any of these mistakes, you can file an amended return using Form 1040-X within three years of the original filing date.

Haven't filed yet? Schedule an appointment with Jose's Tax Service today. We catch these errors before they cost you money. Our tax professionals stay current on every rule change, threshold adjustment, and deduction requirement that impacts New Haven residents.

Visit Jose's Tax Service or call us to book your consultation. Don't leave money on the table this tax season.

Leave a Reply

You must be logged in to post a comment.